The arrival of the digital age has completely transformed communication between people, as well as cultural aspects which have had an impact on the way of doing business and the relationship between businesses and clients. It is a paradigm shift that has made use of mobile technology, which is indispensable for communication, obtaining information and buying and expanding contact networks. In the case of Chile, the Seventh National Survey on Internet Use and Access (2016), developed by Subtel, concluded that there are 12.7 million Internet users in Chile, with the largest regional development in this area. That is, of every 100 Chilean inhabitants, 76 use the internet and 79.2 percent do so through mobile devices.

“Chile has transformed itself into a highly digitalized country, specially between the ages of 18 and 45”

As for the main activities carried out on the internet, social media take the lead with 65 percent of the preferences, followed by 60 percent for the sending and receiving of emails. The previous figures reflect how Chile has transformed itself into a highly digitalized country. Chileans between the ages of 18 and 45 are the most informed age group, and they communicate and are the country’s biggest users of e-commerce (banking, online shopping, online bill payments). This data has forced companies to adapt to the new needs of their customers/users, adapt to new services and open up new business opportunities online, in order to maintain their place among their target audiences. In this way, all companies strive to put themselves at the forefront of digitization. But the question is: where do they begin?

For several years, the focus was shifting from a purely technological perspective, with an emphasis on tools, channels and platforms. It was soon discovered that technology alone failed to change the behavior of stakeholders. As the digital phenomenon has grown, evidence of the importance of communication as an agent of transformation has also grown.

As authors, we asked ourselves which were the three main goals of digital transformation from communication and how brands manage to lead the digital transformation of communication when it surpasses in relevance (OutPut), influence (Out-Take) and beliefs (OutCome) to the referents or competitors of their market or industry.

For this study, we selected 20 brands of the stock market index of the Santiago Stock Exchange, which are significant for their production of digital content and participation in social media, with a presence in the banking, services, retail and wine sectors, among others.

It should be noted that the brands selected are not directly named in the index, understanding that there are groups of companies which did not have any digital identity, so those with the greatest digital activity were selected depending on the company.

The study is based on a temporary sample extracted between February 20 and March 20, 2017, so when analyzing the study, it is necessary to consider the contingency and eventualities that the brands could face during this period.

OutPut: Relevance

The first challenge of digital transformation is the clouding of public communication channels, which are flooded with communication from the producers of new digital media. In this context, competition for stakeholders’ focus time is the initial goal for creating long-term value.

This is where brand relevance represents the output of communication, defined by AMEC as: “What is distributed and received by audiences.” The relevance therefore, can be measured in terms of visibility (reach) of the contents distributed by the company, through the analytical tools of its platform in a specific conversation territory.

For this study, we selected the main web assets of each company, analyzed the impact of their content on the main social media over the past six months, and counted the number of pages indexed by Google.

Out-Take: Influence

The second challenge of digital transformation is the empowerment of people in public communication, through their identity in media and social media. This is a reality that drives the economy of interpersonal recommendation as a lever for creating shared value for companies.

It is at this point that we find the personal influence of the organizations’ allies in social media such as the out-take, which the AMEC defines as: “What audiences do and get from communication.” Influence, therefore, can be measured in terms of the interaction (engagement) of influencers in a community with brand allies.

For this study, we selected the main profiles of each brand on Twitter and Facebook, recording the total number of interactions, respectively, during the last month (March 2017). In addition, we counted the total number of external links pointing to the web domain of each brand.

OutCome: Beliefs

The third challenge of digital transformation is the hyper-transparency of brand behaviors, which are permanently monitored by their stakeholders, through social media and other online platforms. This makes the economy of reputation a key element for the generation who like long-term value.

To improve these beliefs, brands need to investigate the context in which they are placed by interest groups to form their own judgment, which is always done in comparative terms with other referents. Belief metrics conform to measures of assessment (between positive and negative) collected through opinion surveys or through the semantic analysis of opinions on monitoring platforms.

For this study, we analyzed the feeling of the first results on Google of each of the brands and the tweets with the most reach, in addition to the total number of followers on the pages of each brand on Facebook.

Best practices by sectors

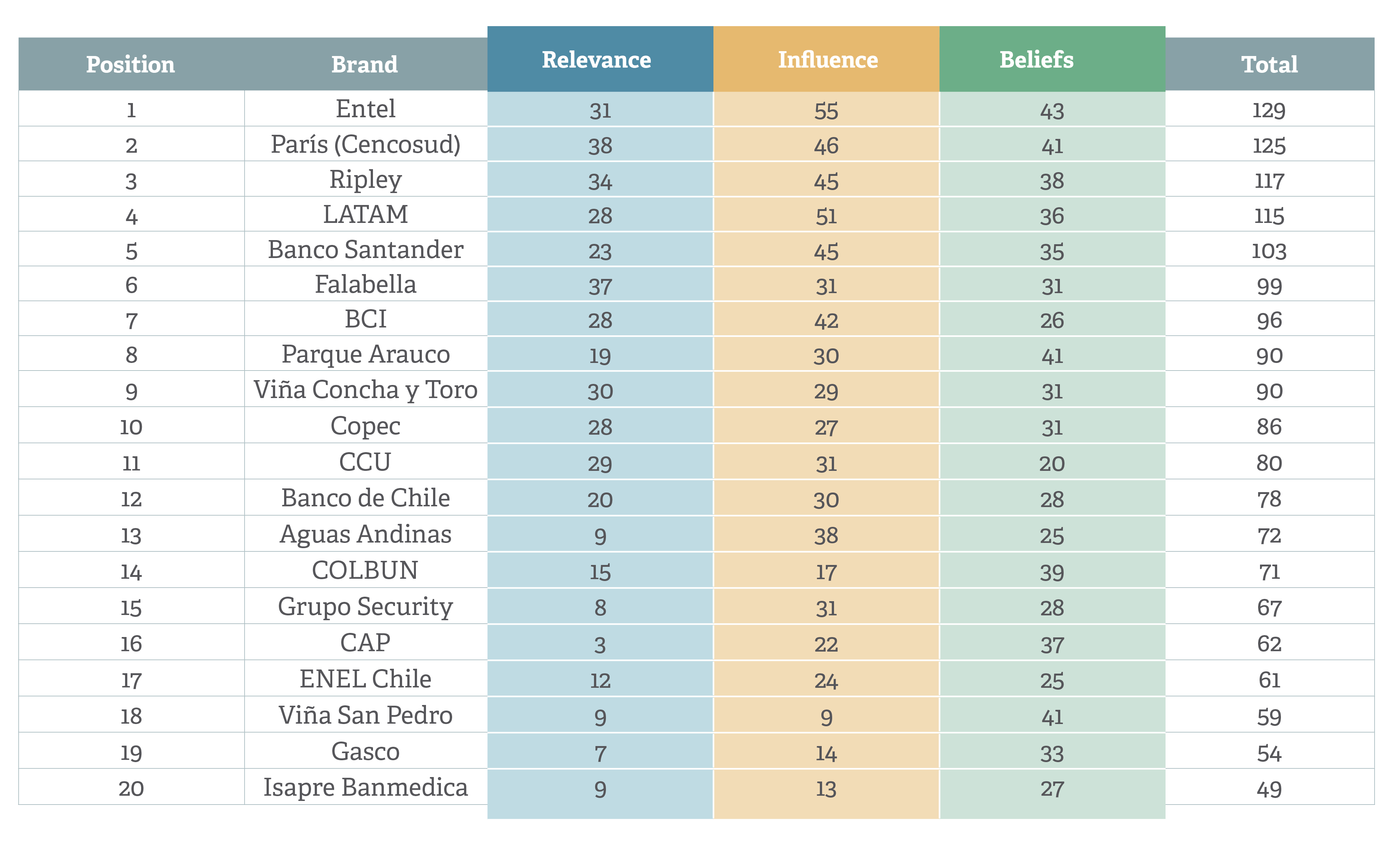

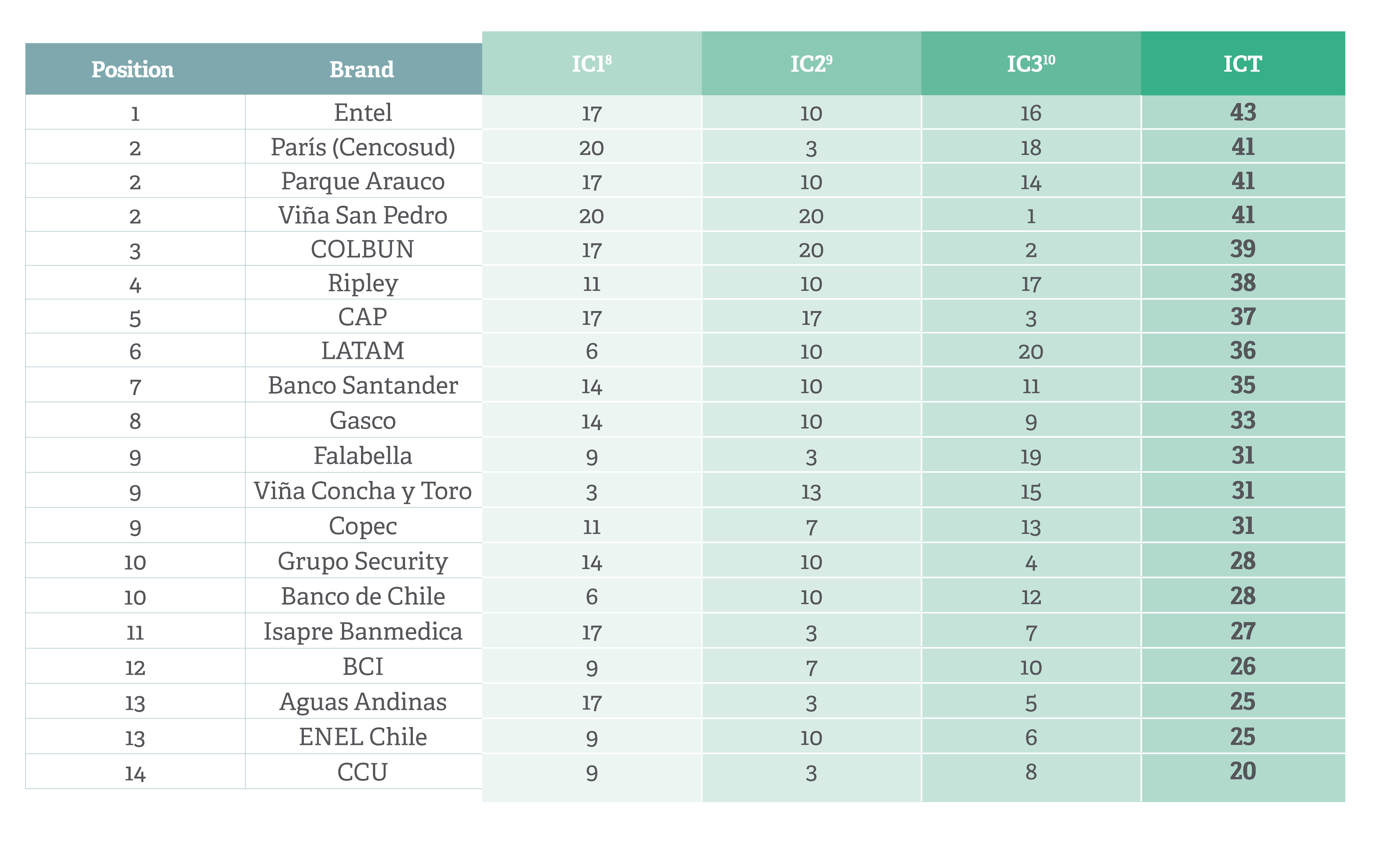

TOP 20 DIGITAL BRANDS

Ver tabla

Entel and Paris (Cencosud) lead the ranking of digital brands in Chile

The goal of leading digital communication in a market is to achieve three objective goals: positioning more content than competitors in networks and search engines (relevance); generating more interactions than others with followers on social media (influence), and; receiving more positive than negative mentions towards the brand, in the main digital environments (beliefs).

“The operator stands out for its greater influence in networks and the distributor for the relevance of its digital content.”

Taking the metrics of this study into account, the following five brands are the top brands in Chile: Entel and Paris (Cencosud); followed by Ripley and LATAM; and slightly further down the list, Banco Santander. At the bottom of the table, we find five other brands with the greatest opportunities for improvement in their digital communication: Isapre Banmédica, Gasco, Viña San Pedro, Enel Chile and CAP. The main weakness they share focus on the poor visibility of their content on search engines, which has repercussions on their relevance metrics. In addition, both Gasco and Isapre Banmédica do not have an official Twitter account, so their participation on the network is passive. The average of the Top 20 Digital Marks is 85 points, a score reached by Copec, surpassed by 4 points by Viña Concha y Toro.

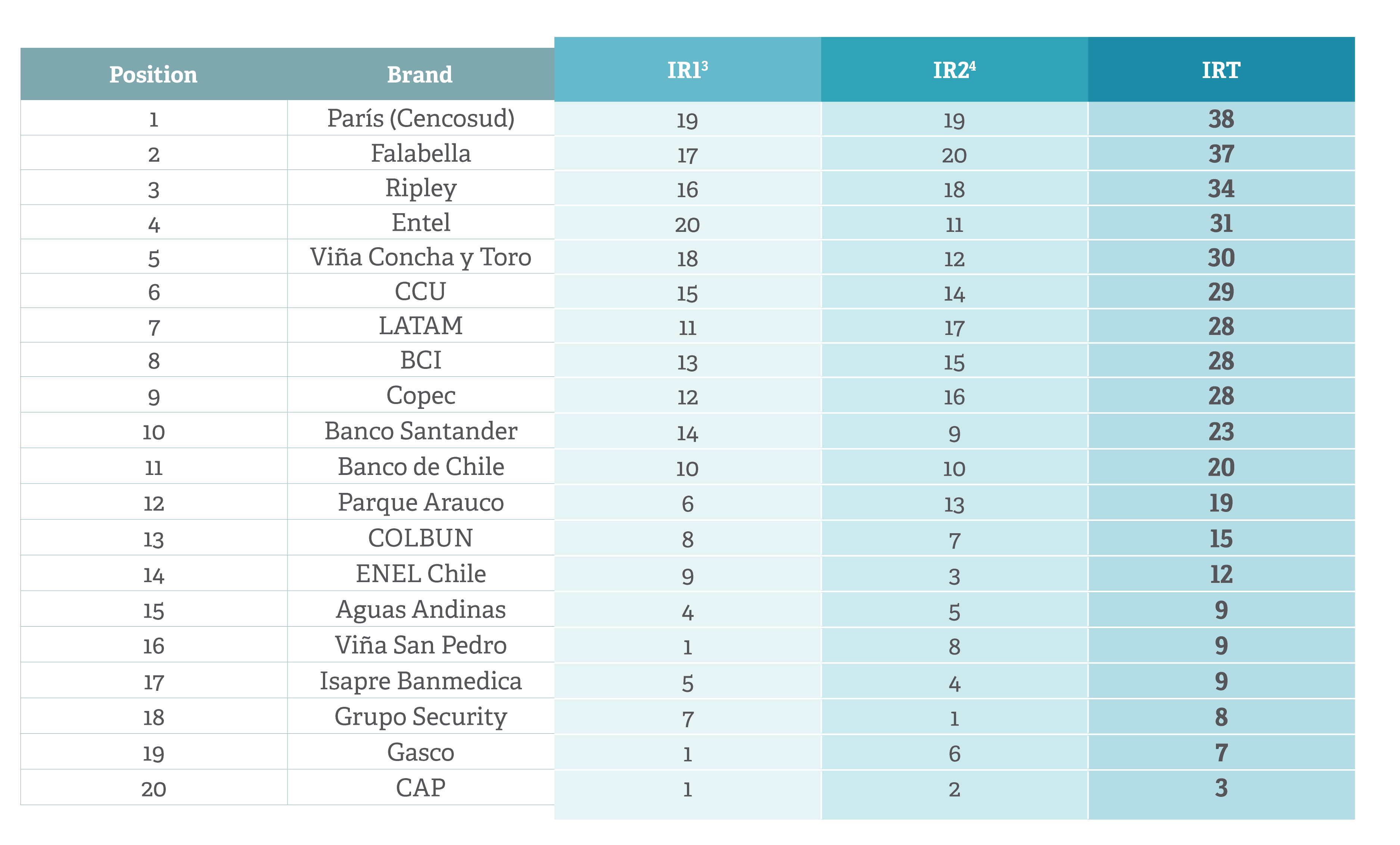

TOP 20 BRANDS BY RELEVANCE

Ver tabla

The retail sector (Paris, Falabella and Ripley) have conquered the podium of digital relevance.

The richness in content of the websites of three of Chile’s leading retail brands (Paris, Falabella and Ripley) has been transformed into greater potential visibility on networks and search engines than that of its competitors in this particular ranking. However, two companies outside the sector are among the five most important: Entel, leader in propagation in social media; and Viña Concha Toro, with a good position in search engines. The average relevance aspect is 21 points.

“They are imposed by the dissemination and positioning of their own content on Twitter, Facebook and Google”

Among the highest ranked companies, LATAM’s position stands out and, above all, so does Banco Santander’s, in the pack of followers of the most relevant brands for the visibility of their contents in networks and search engines. As we will see later, both are among the highest for their interaction on their networks, but this does not imply that their followers share their content beyond the platforms of both brands’ own relationship.

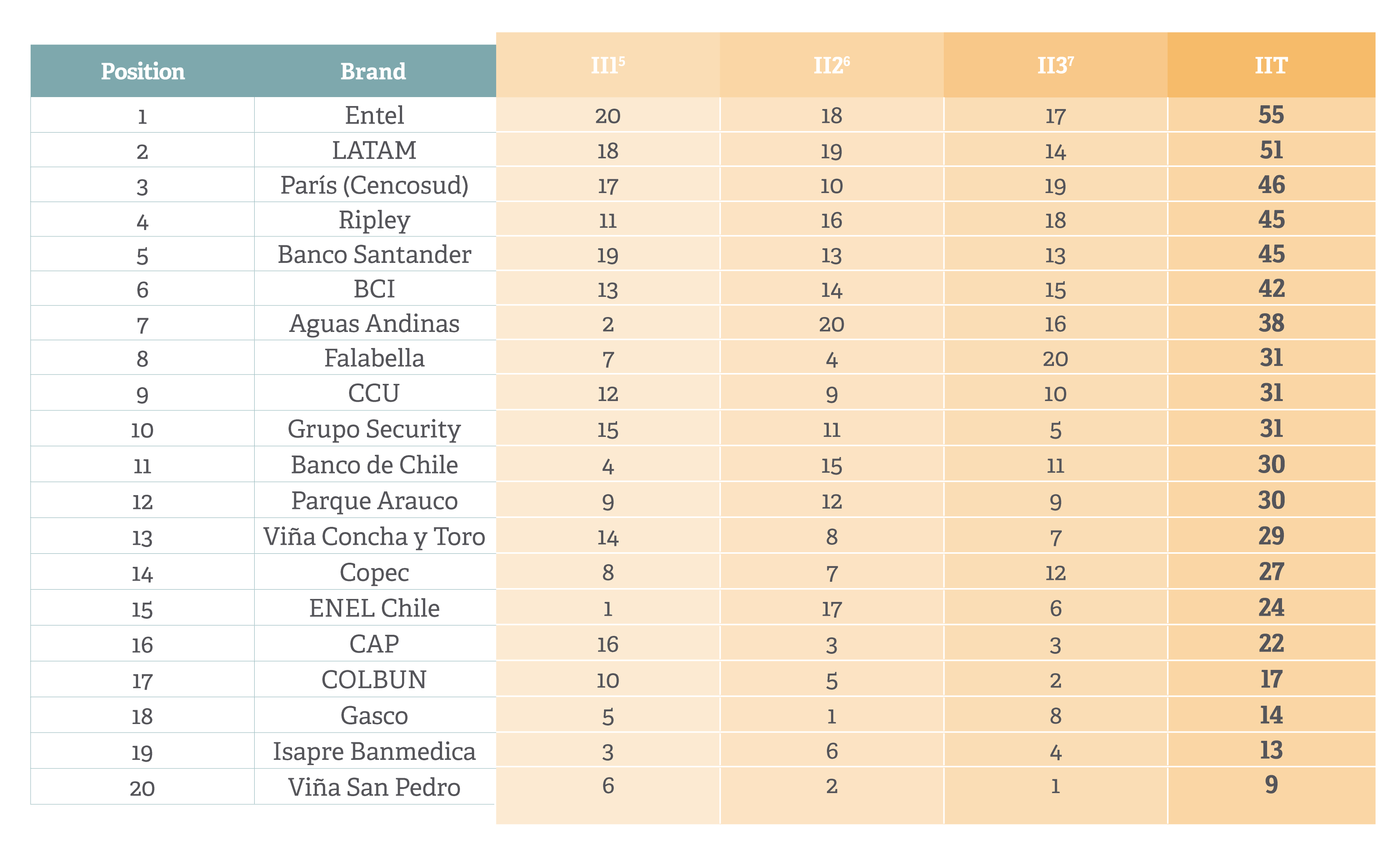

TOP 20 BRANDS BY INFLUENCE

Ver tabla

The leaders of the digital ranking agree on enhancing their influence on social media

The same five brands that lead this digital ranking do so in the variable relative to influence or engagement with their followers. However, this is not the case in the relevance or visibility variable, or in the reputation or belief, where the top five change, except for Entel and Paris (Cenco sud) which are always present among the best on the list in all variables. The average influence aspect is 32 points.

“They concentrate their results on managing interactions with followers of their own channels on Facebook and Twitter.“

This coincidence may indicate a preference for digital strategists to prioritize interaction with their followers in brand channels (community management), over content propagation, through content marketing tactics, to improve their digital positioning, and managing positive ratings through marketing intelligence, to improve their brand reputation.

TOP 20 BRANDS FOR BELIEFS

Ver tabla

Reputation provides opportunities to less relevant and influential brands

While the negative mentions to their brands take LATAM and Banco Santander out of the top five in terms of reputation, other companies located in the middle or low positions of the table by influence and relevance, such as Parque Arauco, Viña San Pedro and COLBUN, manage to rise to the top of the belief ranking thanks to the positive balance of their mentions on Google and Twitter.

“Favorable beliefs include Parque Arauco, Viña San Pedro and COLBUN at the top of the list”

This circumstance indicates the growth potential that is offered to the best rated brands online, to the extent that they are able to capitalize on this value in the form of propagation of relevant digital content and interaction with influential users in the networks.

And conversely, for those with loss of reputational value, it is a managerial challenge to optimize that balance, based on an intelligent active listening of the digital platforms in which they participate.

Best practices by sectors

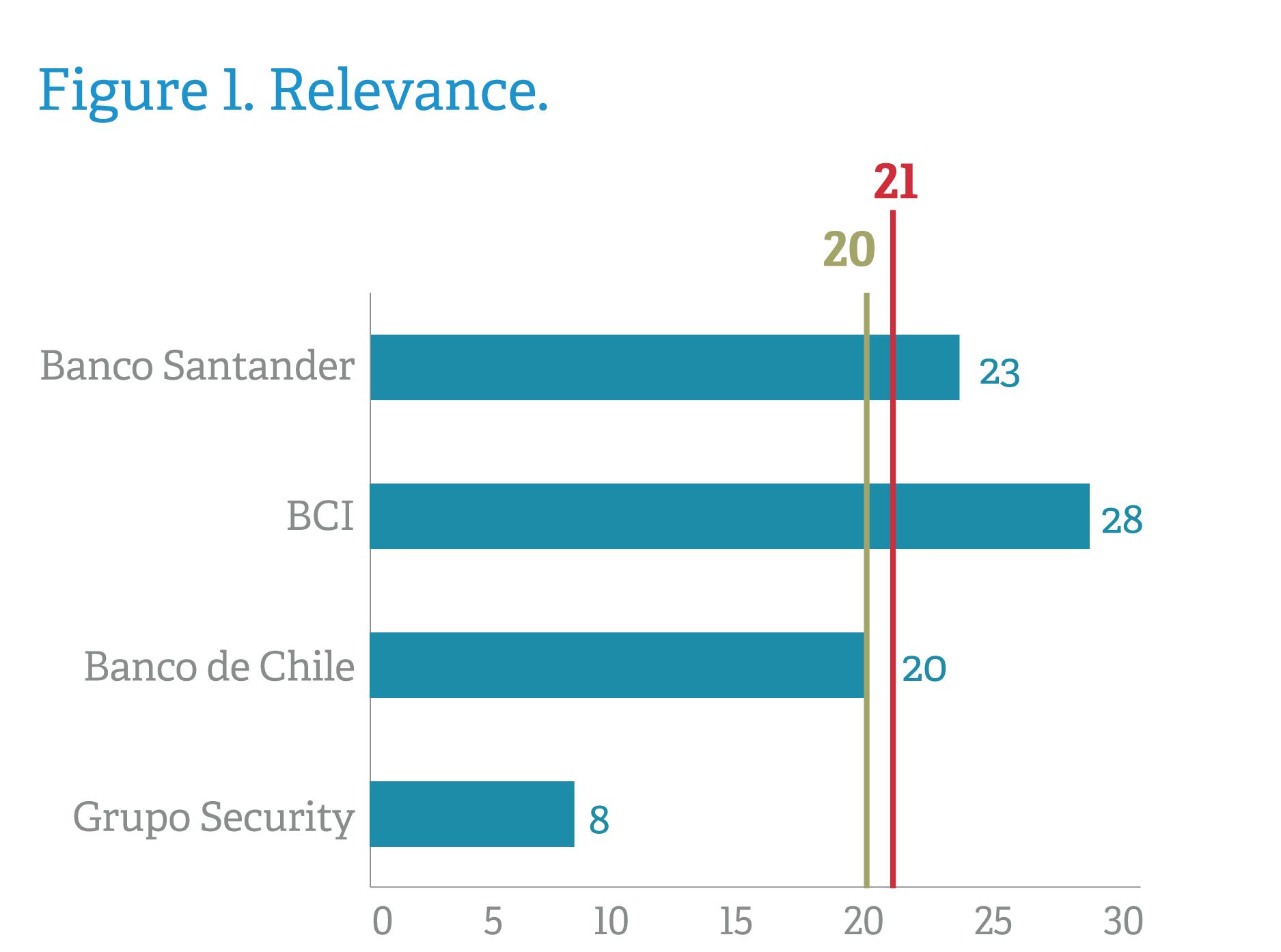

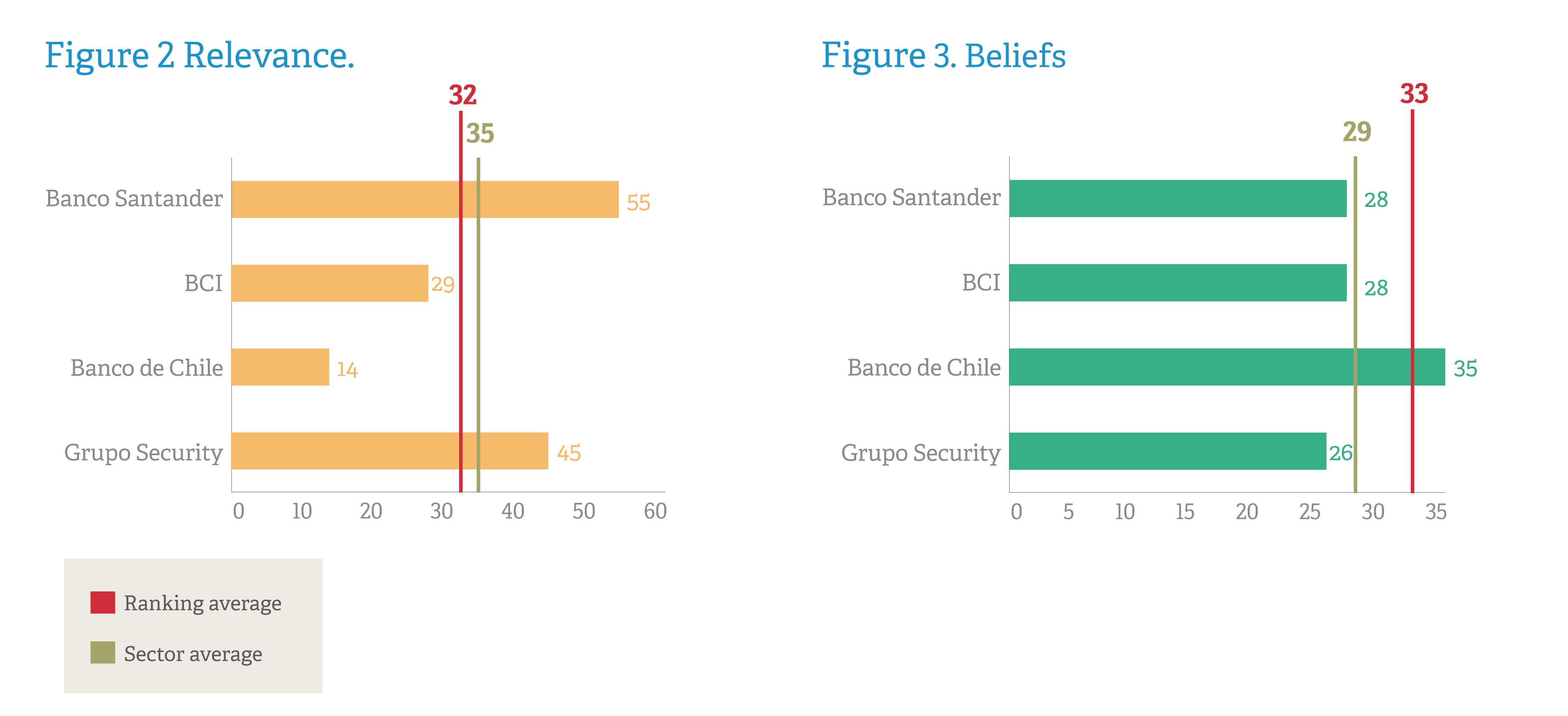

Banking Sector

The banking sector stands out above the average of the ranking for its results in the variable influence, with stand-out exponents such as Banco Santander and Grupo Security. A good use of social media as a means of relationship with the customer, for the provision of services, is noticed.

In terms of content positioning in networks and search engines, it is almost above the average of the study. At the same time, it presents clear areas of improvement in regards of beliefs, for which all the analyzed brands, except Banco Santander, score below the average reputation ranking.

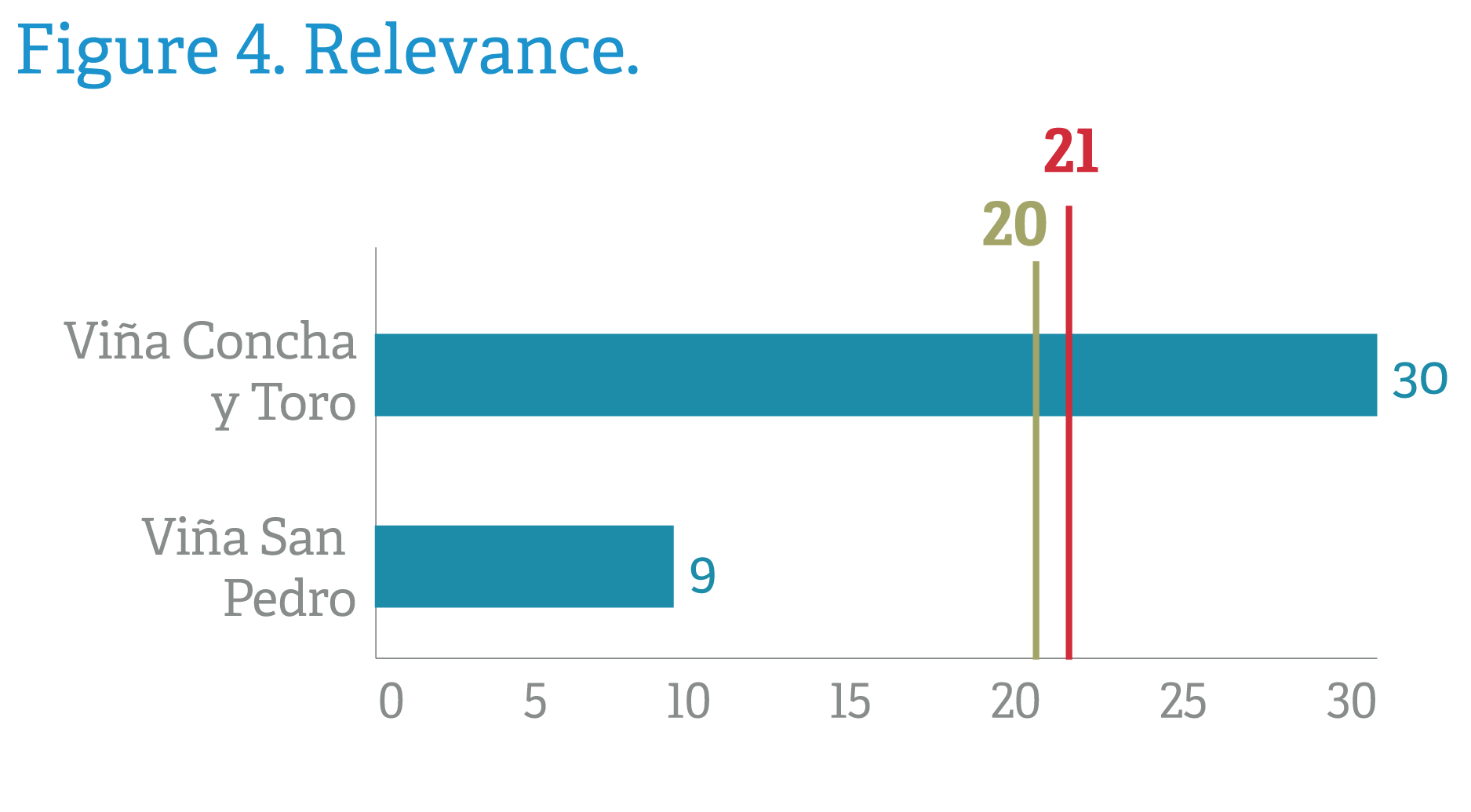

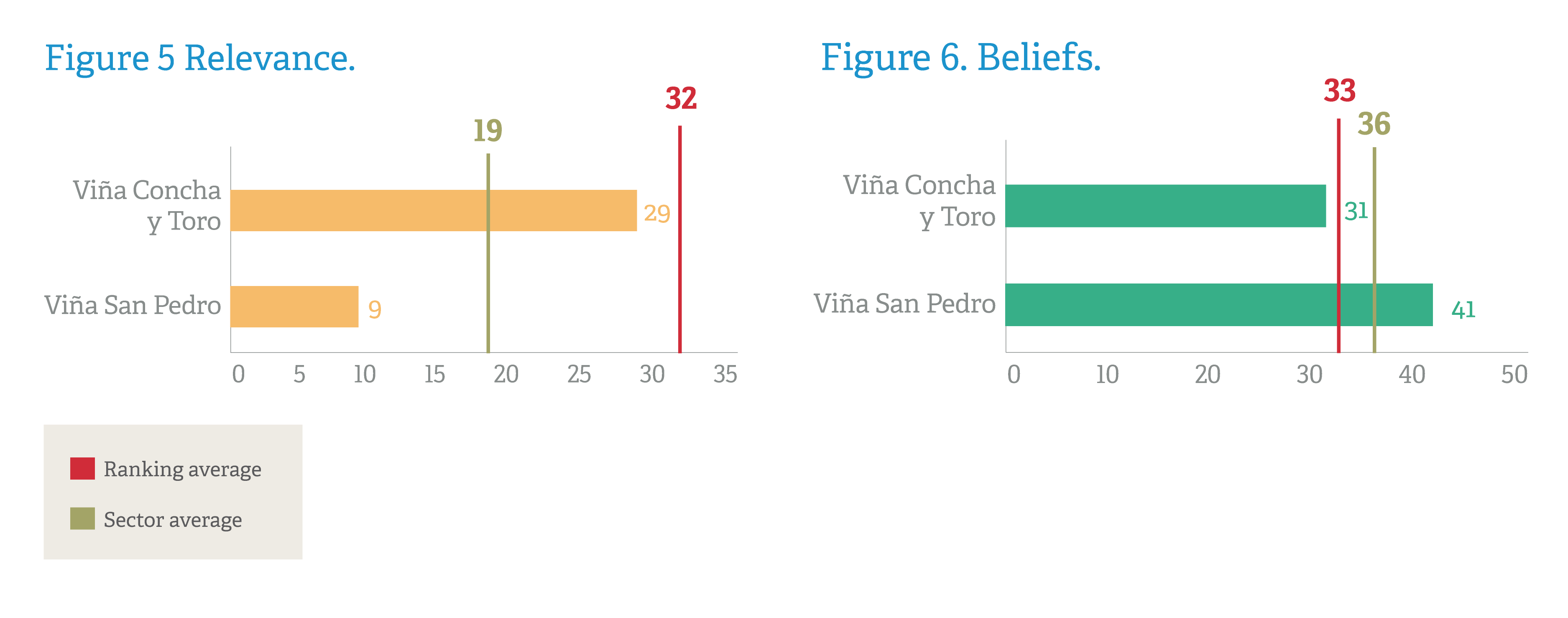

Wine Sector

The results of the wine sector are affected by the disparate behavior of the two brands analyzed in this study. On the one hand, Viña Concha y Toro, with a sum of 90 points, stands five above the average of the brands; while Viña San Pedro, without a presence on Facebook, has a total of 59 points, 26 fewer.

The first stands out because of the relevance of its content, due to external links to its corporate website whilst the latter does so by the positive balance of the mentions it receives on networks and search engines. However, both brands show the same lack of influence on social media. It is striking that their current online communities are relatively small–made up of foreign and English-speaking users.

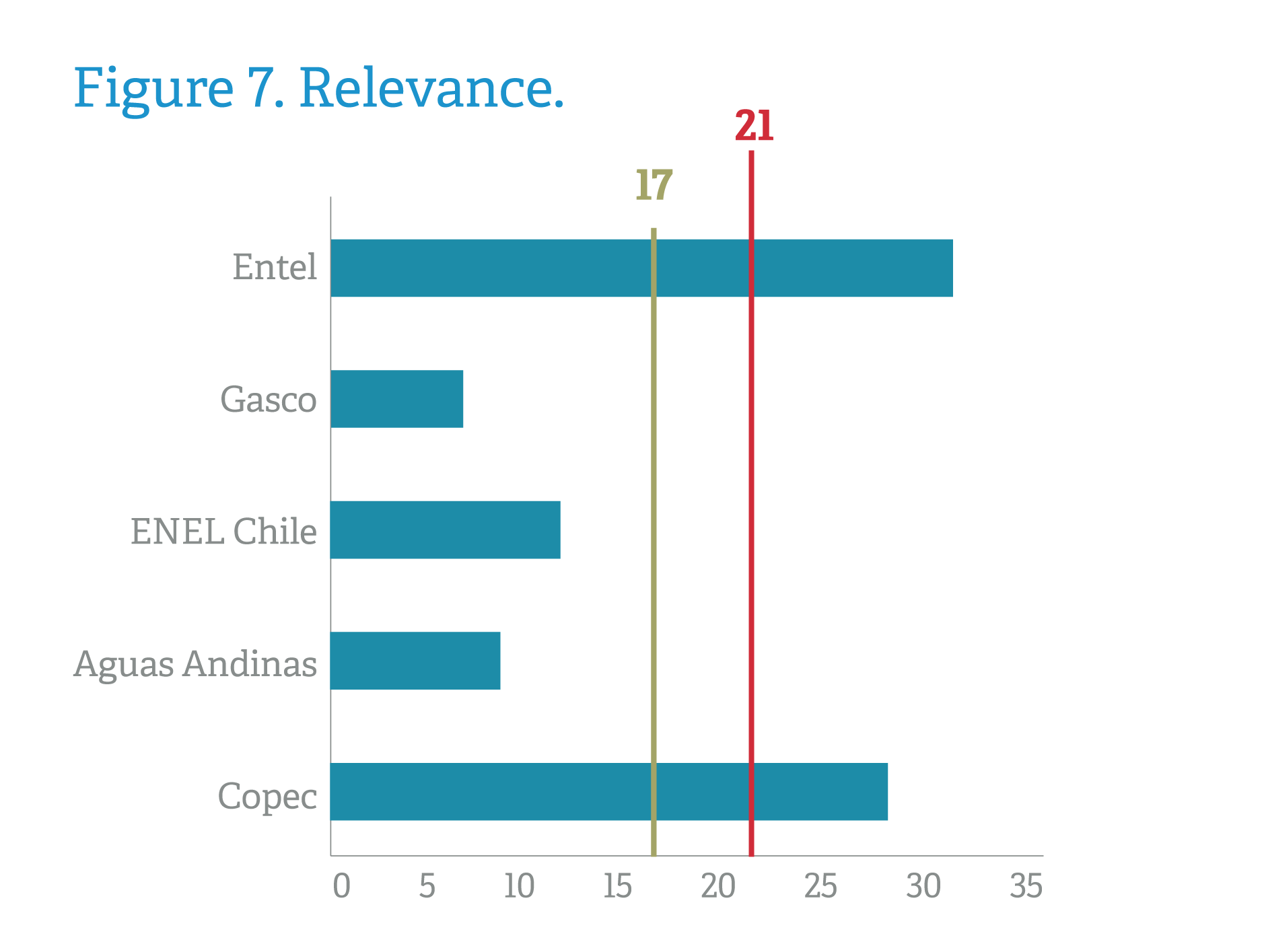

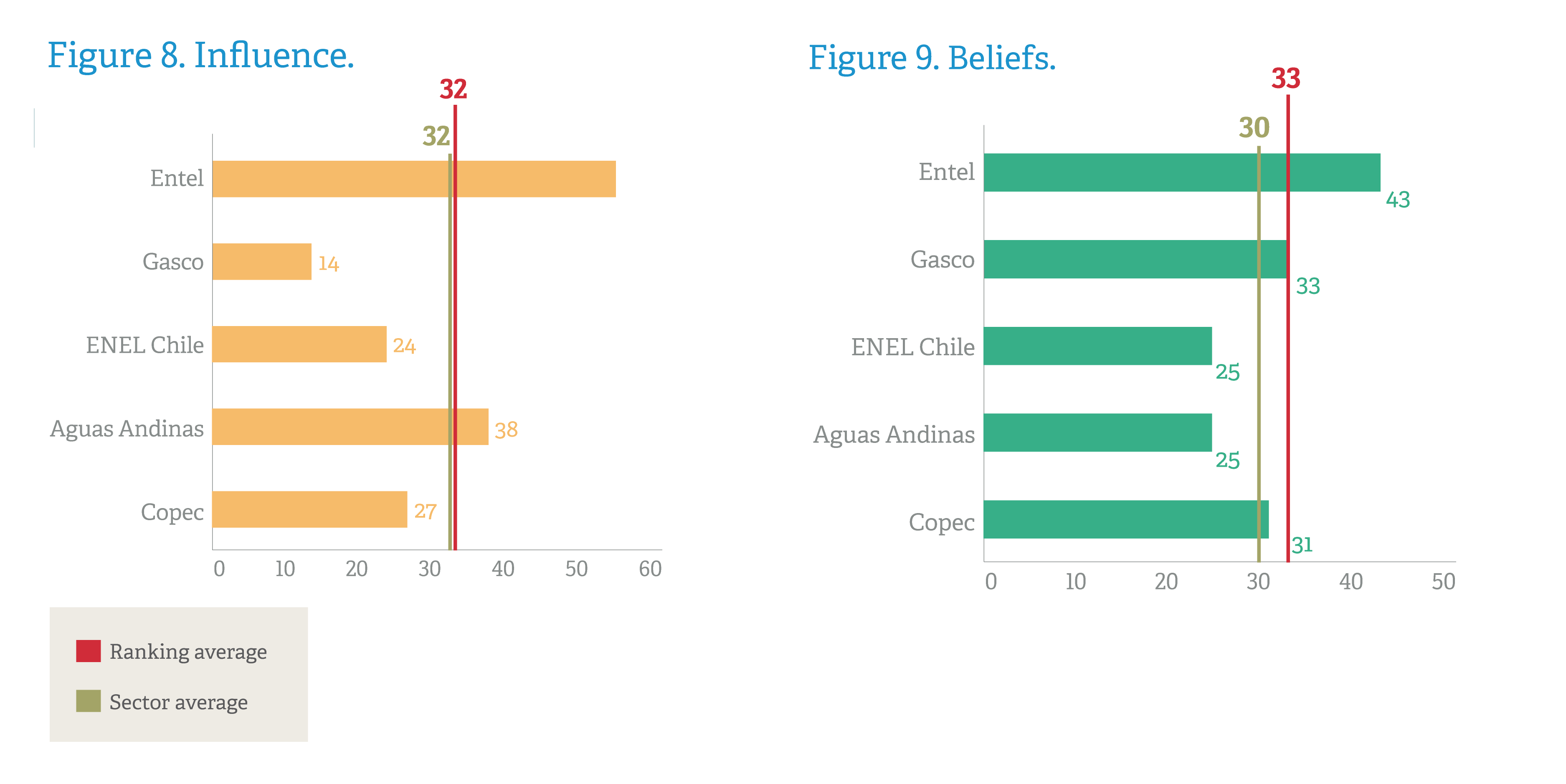

Service Sector

The only variable in which the services sector presents results above the average of the study is in the influence category, by the exceptional number of interactions it generates on social media.

However, the sector average is three points below the ranking average in the other two variables–relevance and beliefs. The brand with the greatest opportunities for improvement is ENEL Chile, with below average indicators in all aspects. While the best-performing brand in the industry is the leader in the ranking–telecom operator Entel.

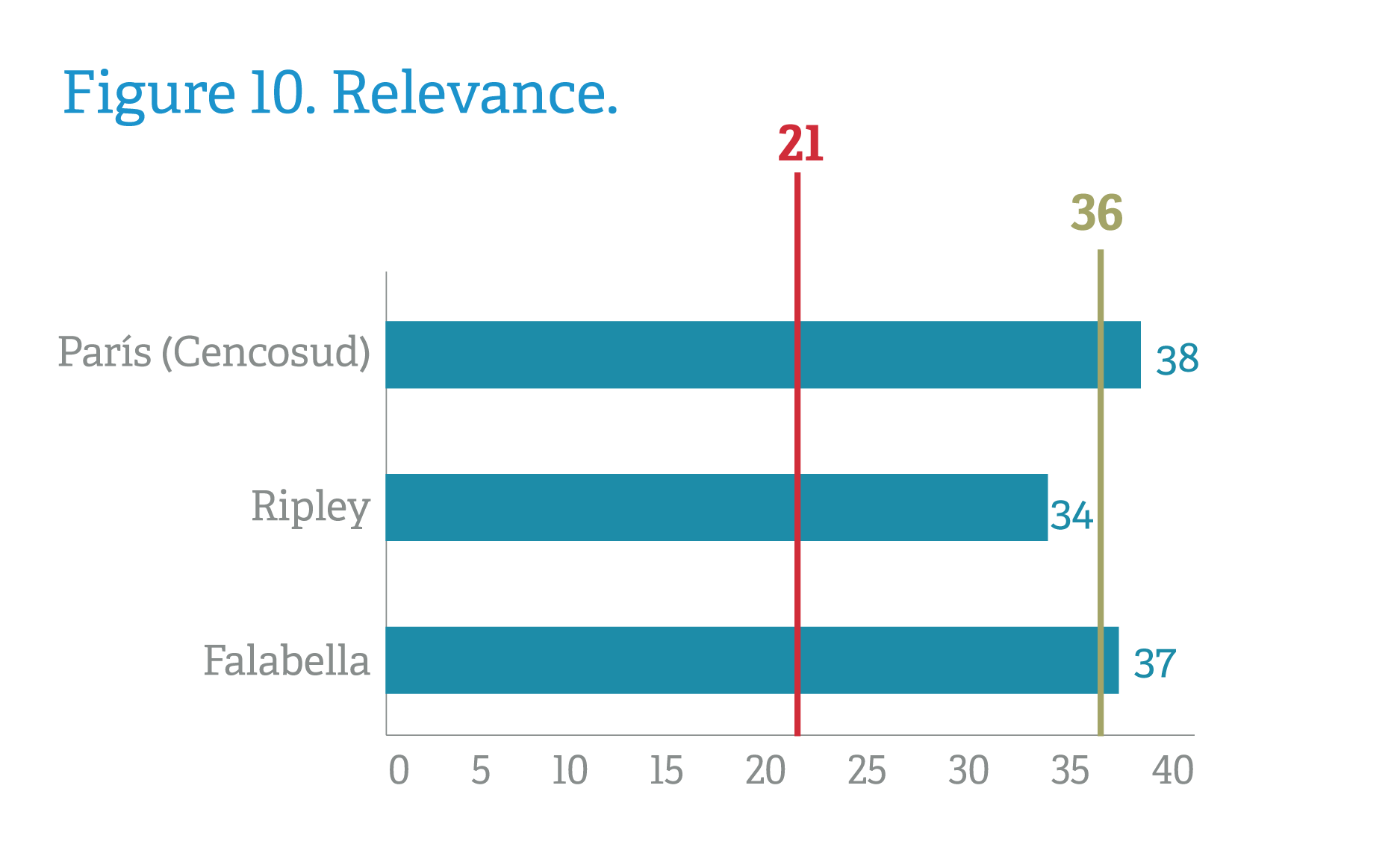

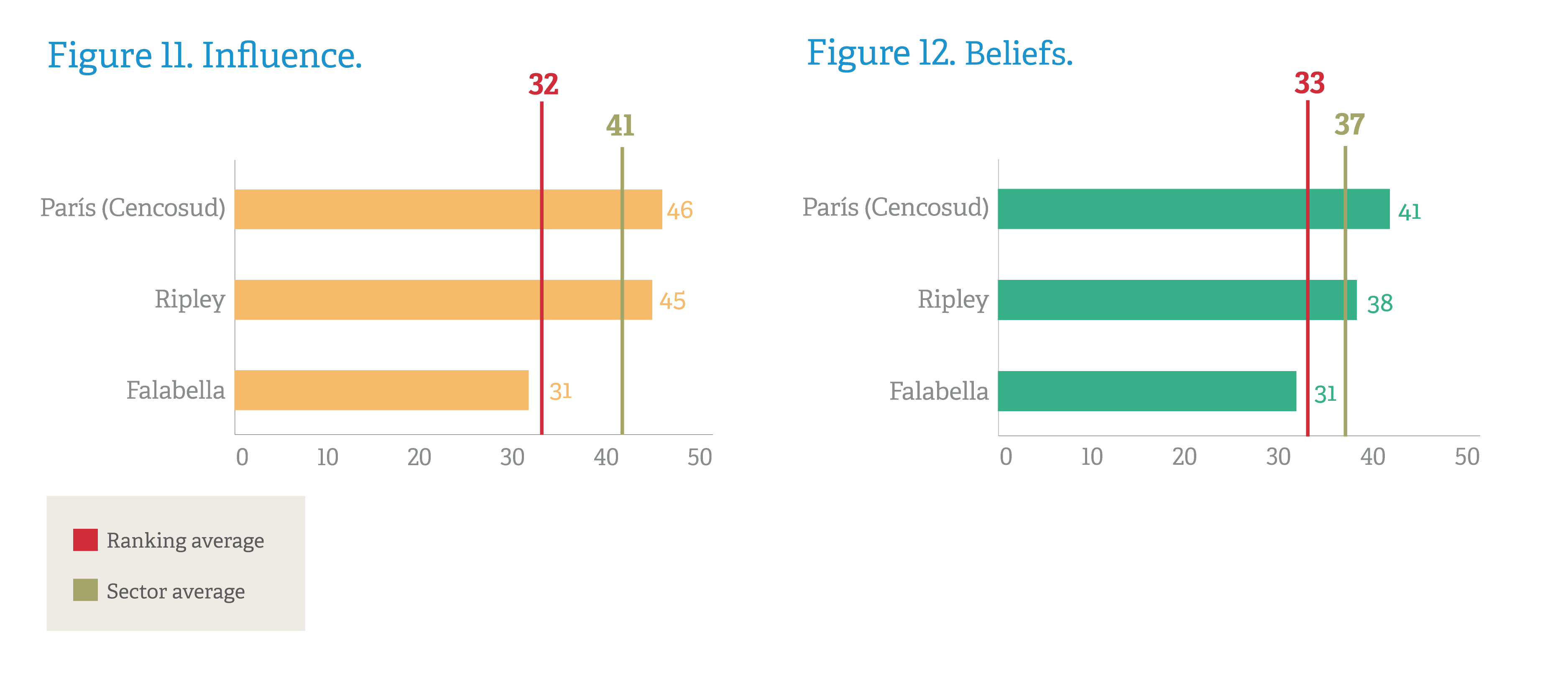

Retail Sector

The retail sector represents the counterpoint of the corporate sector in this ranking in terms of digital efficiency. Their indicators are well above the average of the study in the variables of relevance and influence, demonstrating the dynamism of their participation in social media and effectiveness of the positioning of their web contents. Paris (Cencosud) stands out for these reasons.

The sector’s beliefs index also surpasses the average of the ranking, but a detailed reading warns us about the pressure that brands can suffer from negative mentions related to complaints or service complaints.

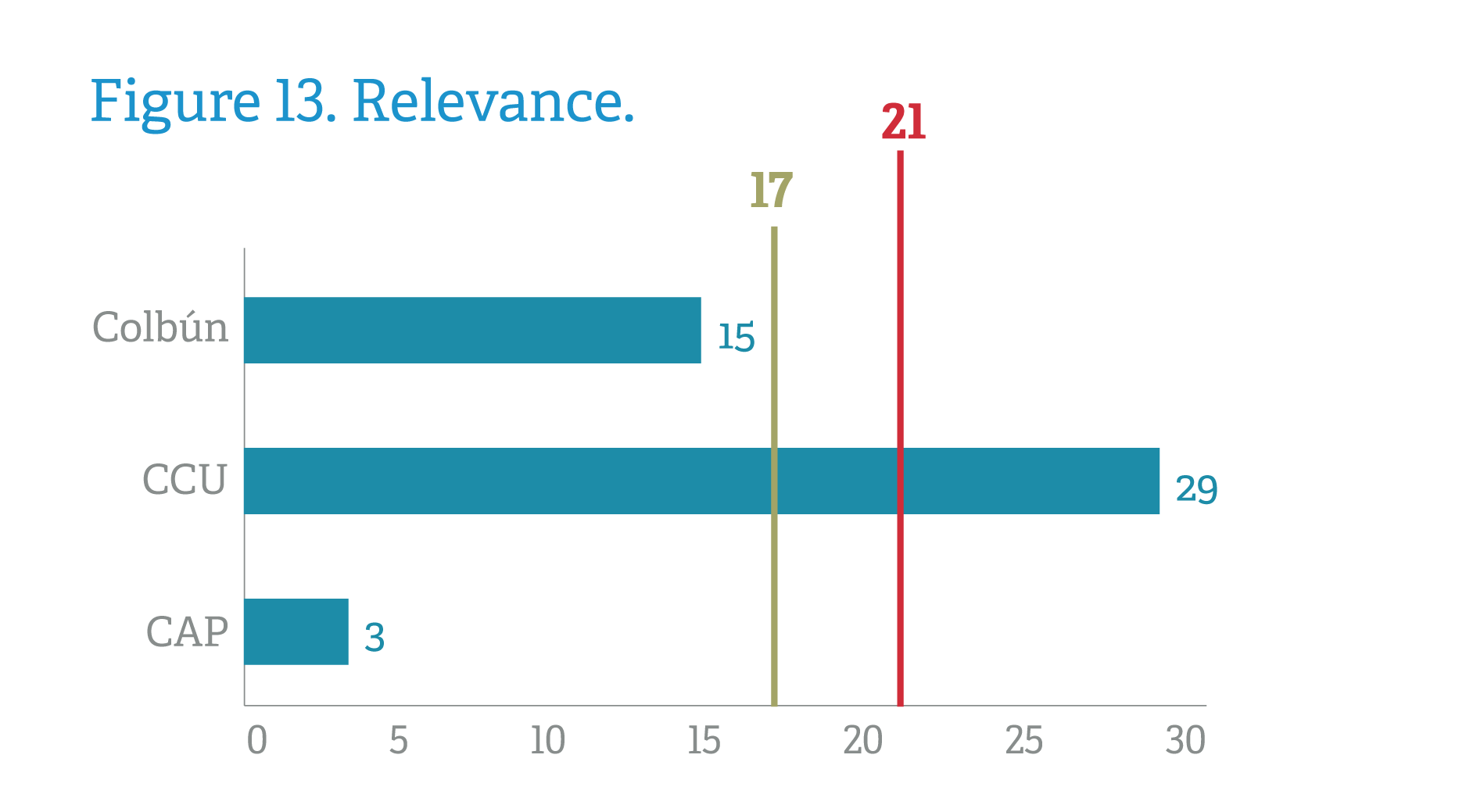

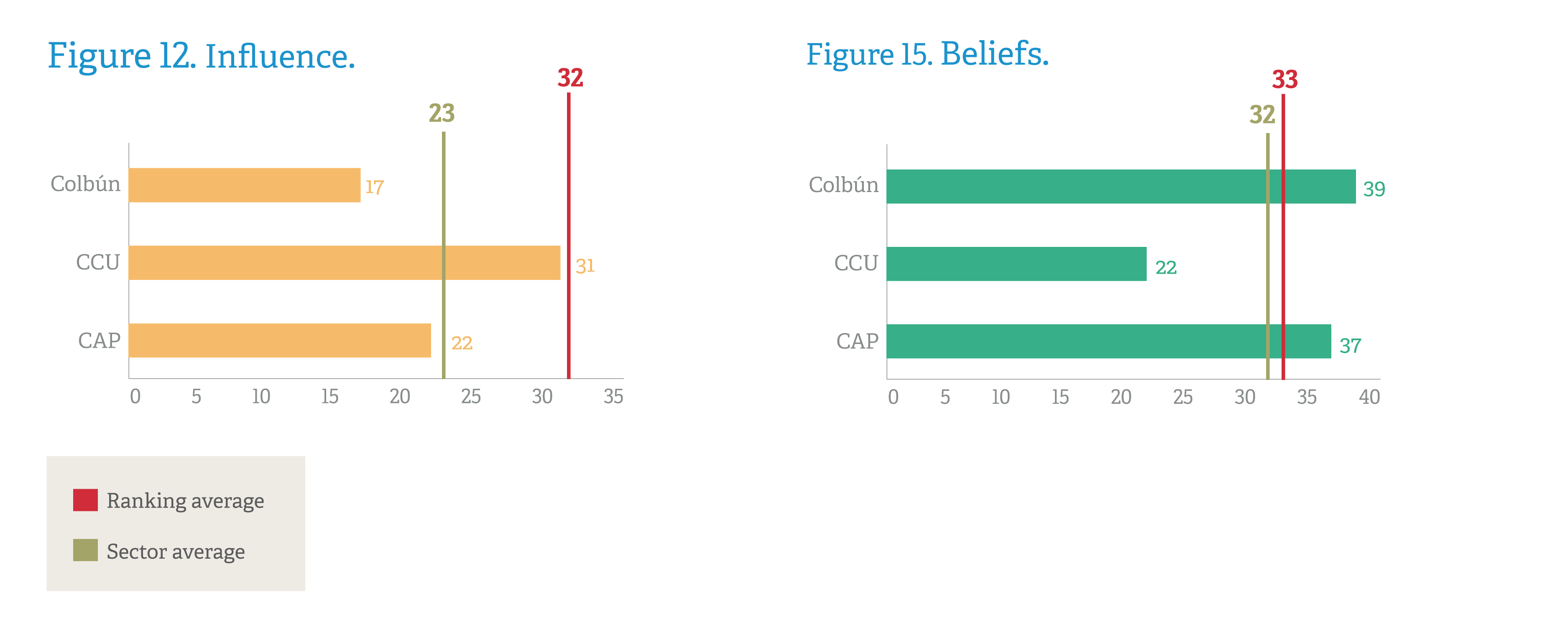

Corporate Sector

The corporate sector is the most deficient in terms of results of the entire ranking. All variables are below average, although only by one point in the case of the belief indicator due to the better positioning of Colbún and CAP in this regard.

Undoubtedly, the main area of improvement of the sector is in the ability to interact with users in social media, as evidenced by the fact that all the brands analyzed are below the average of the study in the influence variable.

Other

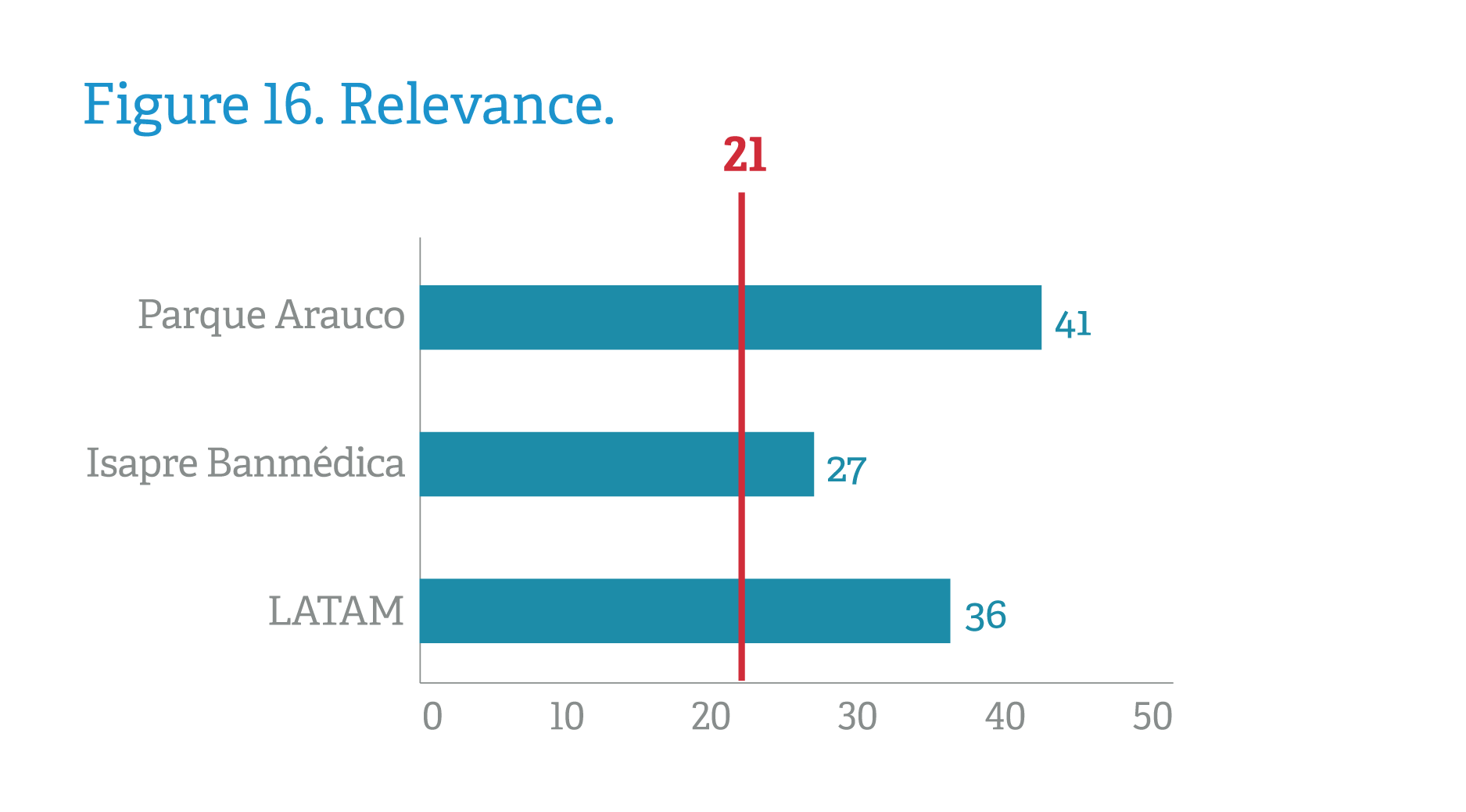

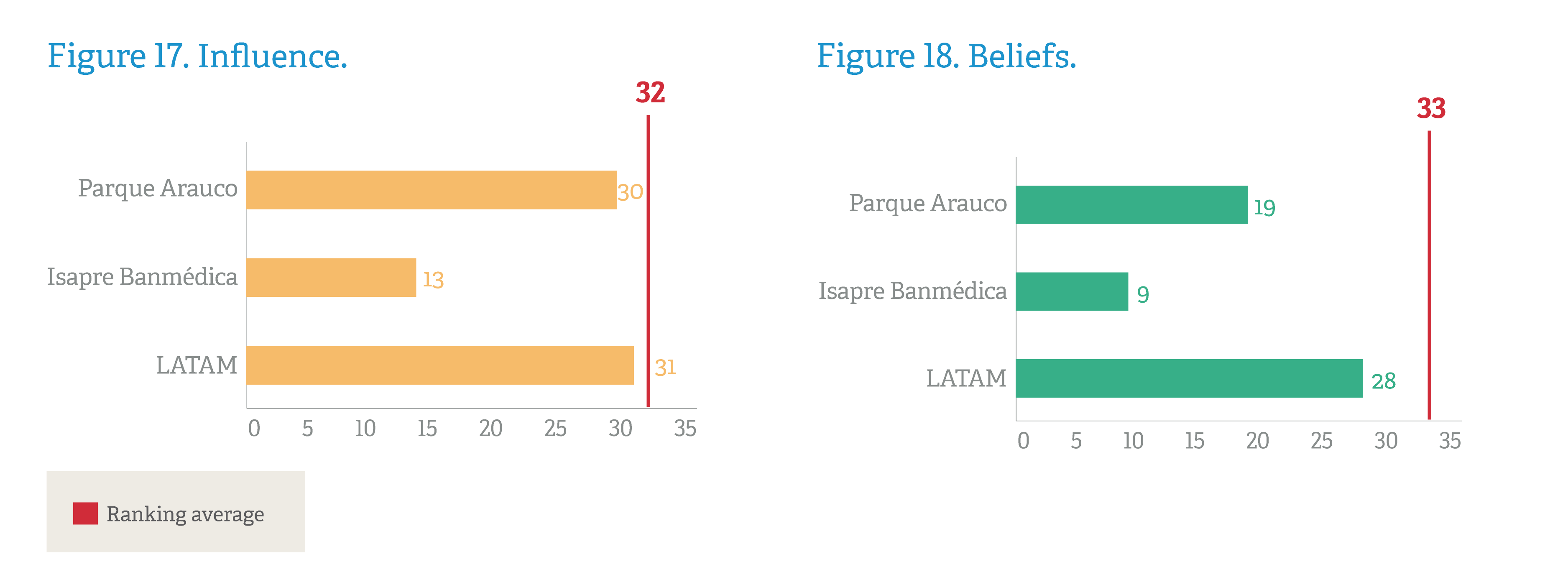

It can be seen that the three brands analyzed in the ranking without other sector referents, Parque Arauco (real estate), Isapre Banmédica (health) and LATAM (airlines) have a very similar behavior in terms of the results.

All three are above average in the ‘relevance’ variable, and below the average in ‘influence’ and above all, ‘beliefs’ variables. It is true that there is a notable distance, however, between the brand with the lowest score of the study, Isapre Banmédica, and one of the best positioned in the ranking–the airline LATAM.

Authors

Néstor Leal is a Director of the Digital Area at LLORENTE & CUENCA Chile. Publicist, with a degree in persuasive communication. He counts with more than 11 years of profesional experience. His work as an interactive should be highlighted and has exercised as a digital director in renowned international and local agencies such as BBDO Chile, Promoplan and iCrossing Latam. He has been responsible for leading the digital strategy for companies such as Mercedes Benz, Sony, Pepsi, Grupo Falabella, among other important brands.